Class 11 Accountancy Mistakes That Become Serious Problems in Class 12

A practical guide for Class 11 commerce students on the accountancy habits and concepts they should fix early so Class 12 does not feel overwhelming.

- 11th

- 12th

- Study Advice

- Accounts

Class 11 Accountancy can feel manageable in small pieces.

One week you learn basic terms. Then journal entries begin. Then ledger, trial balance, depreciation, rectification of errors, and final accounts slowly enter the picture. Many students think, “I will somehow manage this year, and I will become serious in Class 12.”

That is where the problem starts.

Class 12 Accountancy does not begin from zero. Partnership accounts, company accounts, financial statements, and cash flow all expect you to already understand the language of accounts. If your Class 11 basics are weak, Class 12 does not only feel new. It feels confusing from the first month.

The good news is simple: if you know which mistakes matter, you can fix them early. You do not need to become perfect overnight. You only need to stop ignoring the foundation.

Mistake 1: Memorising Entries Without Understanding the Transaction

Many Class 11 students learn journal entries like fixed lines.

“Rent paid means rent account debit, cash account credit.”

That is correct, but it is not enough.

If you only memorise entries, you may manage simple questions for a while. The trouble begins when the wording changes. A transaction may involve credit purchase, drawings, outstanding expense, prepaid expense, depreciation, bad debts, or adjustment entries. In Class 12, questions become longer and more situational, especially in partnership chapters.

Before writing any entry, ask three questions:

- What changed in the business?

- Which accounts are affected?

- Is each account increasing or decreasing?

This one shift makes Accountancy much less mechanical.

Mistake 2: Being Unclear About Debit and Credit Rules

Debit and credit confusion is one of the most common reasons students lose confidence.

Some students remember that debit means increase and credit means decrease. That is only true for some accounts. For assets and expenses, increases are debited. For liabilities, capital, and incomes, increases are credited.

If this is unclear in Class 11, Class 12 becomes stressful because almost every chapter uses debit and credit thinking. Admission of a partner, retirement of a partner, dissolution, shares, debentures, and cash flow all need a clear understanding of what is being recorded and why.

Keep the account type in your mind before applying the rule.

| Account type | Increase | Decrease |

|---|---|---|

| Asset | Debit | Credit |

| Expense | Debit | Credit |

| Liability | Credit | Debit |

| Capital | Credit | Debit |

| Income | Credit | Debit |

Do not only read this table. Use it while solving. If you apply it regularly, it becomes natural.

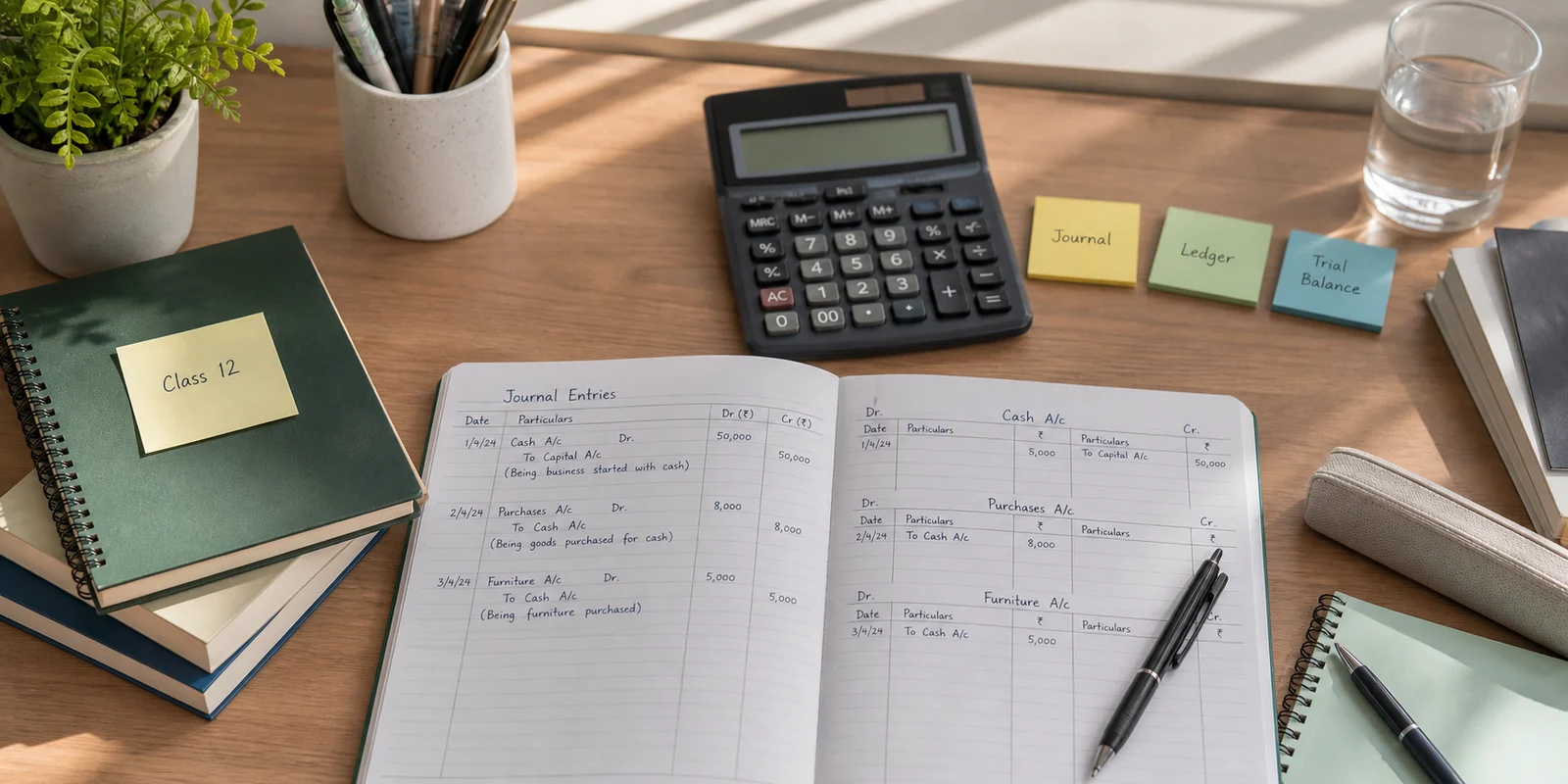

Mistake 3: Treating Ledger Posting as Copying Work

Ledger posting looks simple, so students often do it carelessly.

They copy amounts, write account names, and move ahead without understanding what the ledger is showing. This creates problems later because ledger logic prepares you for capital accounts, current accounts, partners’ accounts, realisation account, cash account, and many other Class 12 formats.

A ledger is not just a neat page. It shows the movement of one account in one place.

For example, cash may appear in many journal entries. The cash account collects all cash-related changes so you can see whether cash increased, decreased, and what the final balance is.

If this difference is clear, Class 12 formats become easier to understand. If it is not clear, every account starts looking like a random table.

Mistake 4: Ignoring Trial Balance Errors

When the trial balance does not match, many students feel irritated and move on.

That is a mistake.

Trial balance is one of the best places to learn accuracy. It shows whether debit and credit totals are equal after posting and balancing. Even when a trial balance matches, some errors may still exist, but if it does not match, it is a clear signal that something needs checking.

Class 12 Accountancy rewards students who can trace mistakes calmly. In long partnership questions, one wrong posting can affect capital accounts, balance sheet totals, and final answers. If you learn error checking in Class 11, you will not panic as easily in Class 12.

When your trial balance does not match, check in this order:

- Recheck totals.

- Check if any amount is posted on the wrong side.

- Check if an account has been missed.

- Check if a figure was copied incorrectly.

- Check opening balances and closing balances.

Mistake 5: Not Building Neat Working Habits

Messy work may not look like a serious problem in Class 11.

In Class 12, it becomes a serious problem.

Long questions need clear formats, working notes, calculations, ratios, adjustments, and final accounts. If your rough work is scattered, you may know the concept but still lose marks because you cannot track your own answer.

Start writing neatly now.

This does not mean your notebook has to look decorative. It means your work should be easy to check.

Use:

- proper headings

- clear account names

- enough space between formats

- working notes for calculations

- one line for one idea

- clear correction marks when you revise

Neat work protects you from careless mistakes.

Mistake 6: Avoiding Depreciation Until the Exam

Depreciation is often treated as one more Class 11 chapter.

But the idea behind depreciation returns later. It helps students understand asset values, adjustments, profit calculation, balance sheets, and cash flow treatment. If you do not understand why assets lose value and how depreciation is recorded, final accounts can feel weak.

Focus on the meaning first.

Depreciation is the reduction in the value of an asset due to use, passage of time, or wear and tear. It is recorded because the business should not show the asset at its original cost forever when part of its usefulness has already been consumed.

Once the idea is clear, methods become easier.

You should know:

- why depreciation is charged

- how it affects profit

- how it affects asset value

- the difference between straight line method and written down value method

- how provision for depreciation works, if taught in your school

Class 12 does not become easier because you memorised depreciation. It becomes easier because you understand how an adjustment affects more than one place.

Mistake 7: Reading Adjustment Words Too Fast

Accountancy questions often hide the real work in small words.

“Outstanding”, “prepaid”, “accrued”, “received in advance”, “on credit”, “cash”, “goods withdrawn”, “bad debts”, “further bad debts”, “provision”, “closing stock” and similar words can change the entire treatment.

Students who read too fast make avoidable mistakes.

In Class 12, adjustment language becomes even more important. Partnership questions may mention goodwill, reserves, accumulated losses, revaluation, unrecorded assets, liabilities, interest, salary, commission, capital adjustment, and final settlement. If you have not trained yourself to slow down in Class 11, Class 12 questions feel overloaded.

Make it a habit to underline adjustment words before solving.

The student who reads the question properly often solves with more confidence than the student who rushes.

Mistake 8: Skipping Rectification of Errors

Rectification of errors can feel detailed in Class 11, but it is very useful.

It teaches you how mistakes happen and how they are corrected. Wrong amount, wrong account, wrong side, complete omission, partial omission, compensating errors, and suspense account are not only exam topics. They train your mind to think carefully about accounting records.

In Class 12, you need this thinking when you check long solutions.

If your balance sheet does not tally, you should not feel helpless. You should know how to inspect the answer step by step.

Rectification teaches that mistakes have patterns. Once you can identify the pattern, correction becomes easier.

Mistake 9: Studying Final Accounts Only as a Format

Final accounts are not just a format to memorise.

Trading account, profit and loss account, and balance sheet show the result and position of the business. If you only memorise where items appear, you may struggle when adjustments are added.

Understand the purpose:

| Statement | What it shows |

|---|---|

| Trading Account | Gross profit or gross loss |

| Profit and Loss Account | Net profit or net loss |

| Balance Sheet | Assets, liabilities, and capital position |

Final accounts help you connect many earlier chapters. Journal entries, ledger balances, trial balance, depreciation, provisions, closing stock, outstanding expenses, and prepaid expenses all meet here.

This is why final accounts are a bridge to Class 12. Partnership accounts and company financial statements are easier when you already understand how a business result and financial position are prepared.

Mistake 10: Not Keeping an Error Log

Most students make the same mistakes again and again because they never record them.

They solve a question, check the answer, feel bad, correct it, and forget the reason. After a week, the same mistake returns.

An error log solves this.

Make a simple table:

| Date | Chapter | Mistake | Correct habit |

|---|---|---|---|

| 17 May | Journal | Treated credit purchase as cash purchase | Read whether payment happened now or later |

| 19 May | Ledger | Posted amount on the wrong side | Check the opposite account rule before posting |

| 21 May | Final Accounts | Forgot outstanding salary | Underline all adjustments before starting |

Read this log before every test. It will show you exactly where your marks are going.

This habit is extremely useful in Class 12 because the questions are longer and the same weak habits cost more marks.

How to Fix These Mistakes Before Class 12

You do not need to redo the whole year in one week.

Start with the topics that carry the most weight into future learning:

- basic accounting terms

- accounting equation

- debit and credit rules

- journal entries

- ledger posting

- trial balance

- depreciation

- rectification of errors

- final accounts with adjustments

Give each topic a small revision slot. Solve questions by writing, not by reading solutions. Accountancy improves when your hand, eyes, and mind work together.

A simple weekly rhythm can help:

| Day | Focus |

|---|---|

| Monday | Revise one concept |

| Tuesday | Solve five short transactions |

| Wednesday | Practise ledger or trial balance |

| Thursday | Redo one old mistake |

| Friday | Practise one adjustment-based question |

| Saturday | Review your error log |

| Sunday | Rest or light revision |

This is not about studying all day. It is about staying connected with the subject.

What Parents Should Notice

Parents often see only marks, but Accountancy understanding is visible in other ways too.

A student may be struggling if they:

- avoid written practice

- say they understood in class but cannot solve alone

- copy solutions without knowing the reason

- panic when the trial balance does not match

- leave adjustment questions blank

- keep making the same entry mistakes

- become unusually slow in long questions

At this stage, support should be calm and practical. The student may not need pressure. They may need structure, regular checking, and someone to explain the concept in a way that finally makes sense.

Class 11 is the right time to fix this because there is still space to slow down and rebuild.

Final Thought

Class 12 Accountancy becomes much easier when Class 11 basics are not treated casually.

You do not have to be the fastest student in the class. You do not have to solve every question perfectly on the first try. But you do need honest practice, clear concepts, and the habit of correcting mistakes properly.

If your Class 11 Accountancy feels weak right now, do not panic. Start with journal, ledger, trial balance, depreciation, rectification, and final accounts. These are the roots. Once the roots become stronger, Class 12 Accountancy feels far less frightening.

Frequently Asked Questions

Is Class 11 Accountancy really important for Class 12?

Yes. Class 12 has many new chapters, but the thinking comes from Class 11. Debit and credit, journal entries, ledger logic, adjustments, and final accounts all help you understand Class 12 questions more easily.

Which Class 11 Accountancy topics should I revise before Class 12?

Revise basic terms, accounting equation, debit and credit rules, journal entries, ledger posting, trial balance, depreciation, rectification of errors, and final accounts with adjustments. These topics build the strongest base.

What if I passed Class 11 but my basics are weak?

You can still improve. Do not try to revise everything at once. Start with journal entries and ledger posting, then move to trial balance and final accounts. Practise a little every day and keep an error log.

Why do I understand Accountancy in class but make mistakes at home?

This usually happens when you follow the teacher’s solution but do not practise enough independently. After class, solve a similar question without looking at the answer. That is when real understanding becomes visible.

How much daily practice is enough for Class 11 Accountancy?

For most students, 30 to 45 minutes of focused written practice is more useful than long, irregular study sessions. The key is consistency, correction, and understanding why mistakes happen.

Should parents worry if a student is making mistakes in Class 11 Accountancy?

Mistakes are normal in a new subject. Parents should worry only if the same mistakes keep repeating and the student avoids written practice. Early support can prevent small gaps from becoming Class 12 stress.

Looking for commerce tuitions?

Prachi is a gold-medalist commerce teacher with experience at Deloitte and KPMG. She focuses on fundamentals to build a strong foundation.